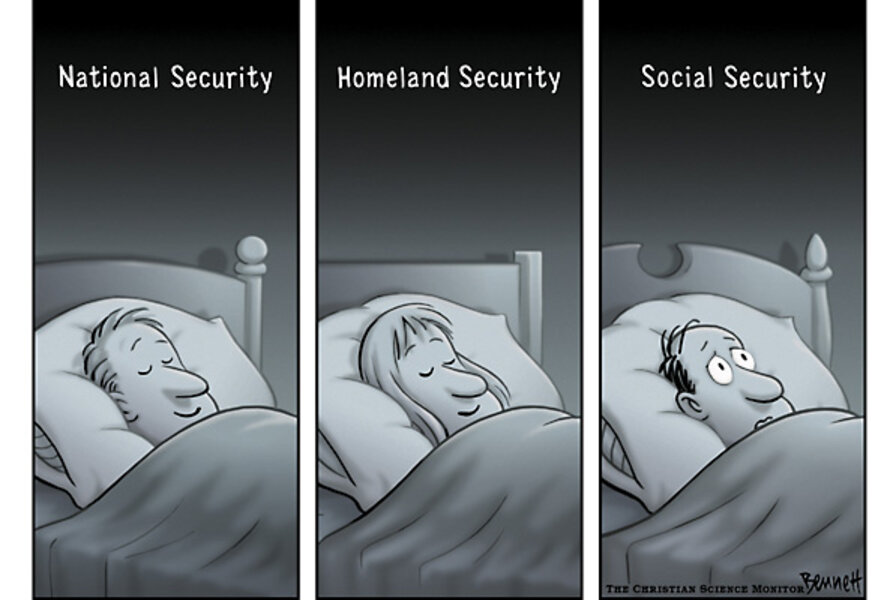

Social Security? Don't count on it.

This is a message to all of those people under, say, forty out there.

Don’t rely on Social Security for any part of your retirement. When you’re thinking about retirement, assume that you’re going to be paying your own way.

That’s not a statement that a lot of people like to think about, but the data pretty much points to this as an inevitability. Let me explain why.

Take a look at the birth rate by year in the United States. During the years when the “baby boomers” were arriving on the scene (the early 1950s, for example), you saw a birth rate of 25 babies per 1,000 people in the population. By the 1970s, this birth rate had dropped to 15 babies per 1,000 people in the population and never really recovered. In fact, the current birth rate is the lowest it’s ever been – 13.5 babies per 1,000 people.

To put it another way, the age of the average American is rising. According to this data, the average American is about 0.2 years older each year and is currently 36.7 years old.

With the population getting older and with fewer babies being born, you have more people reaching retirement age with less people entering the workforce. That means more people are moving to the point of taking money out of Social Security and fewer people are joining the workforce to pay into Social Security.

What happens to any pool of money if you suddenly start paying out more than you’re paying in? It dries up. The sheer numbers say that’s what’s going to happen to Social Security.

Well, why can’t something change? The problem with touching Social Security in its current form is that it’s a political nightmare. Politicians are afraid to touch the issue because people who are retired and receiving Social Security benefits are also the people who often have the most time to vote and to get involved in political causes.

There aren’t very many ways that this problem can be solved. The most likely solution will be to simply raise the benefits age for Social Security – and raise it again – and raise it again. What that would mean is that by the time we retire, we’ll have to be very, very old before we see Social Security money.

What that means is that unless we want to work until we’re in our eighties, we’d better start planning for our own retirement now, not later.

Even if this doesn’t come to pass and a great new solution somehow solves the Social Security problem, saving for your own retirement is still incredibly beneficial, because it allows you to have financial means in retirement that go far beyond the small Social Security benefits.

What can you do? It’s simple. Start saving for retirement now, whether you’re 22 or 35. The earlier you start, the better off you are.

If you have a 401(k) plan at work, that’s usually a good place to start. If your employer matches your contributions, that’s even better. Don’t worry about not knowing anything about investing – it’s far more important to start contributing than to find the “perfect” investment. Head over to your benefits office and get this set up today.

If you don’t have a 401(k) (or a 403(b) or something similar) at work, you can do it yourself by setting up a Roth IRA. It’s really easy to do – just open an account at an investment house (I use Vanguard) and set up an automatic contribution out of your checking account.

Think of it as a little thing you can do right now to help your future self a lot when he or she is in their sixties. Giving up a magazine subscription or something else small now can give you the freedom to control your own destiny when you’re older. That’s a great trade if you ask me.

Add/view comments on this post.

------------------------------

The Christian Science Monitor has assembled a diverse group of the best economy-related bloggers out there. Our guest bloggers are not employed or directed by the Monitor and the views expressed are the bloggers' own, as is responsibility for the content of their blogs. To contact us about a blogger, click here. To add or view a comment on a guest blog, please go to the blogger's own site by clicking on the link above.