Revisiting oil and natural gas prices

My recent post about oil and natural gas prices elicited some very constructive responses from readers (thanks in particular to PJ, MF, and FW, in addition to public commenters on the post). As a result, I’ve rethought my discussion of the relationship between oil and natural gas prices.

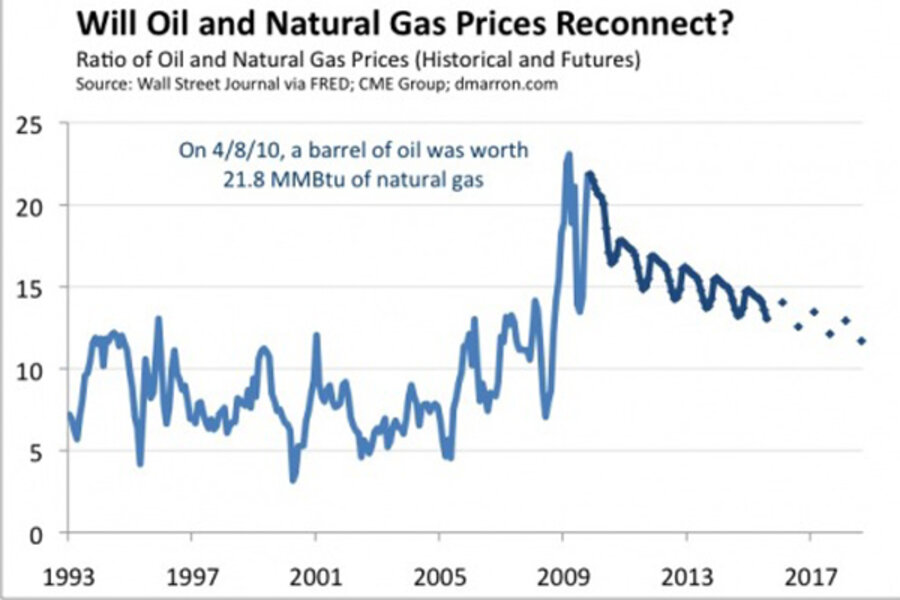

I was also inspired to look at the futures markets to see what they are signaling about the relationship between oil and natural gas prices. Here’s my usual chart of the ratio of oil prices to natural gas prices (see chart above), now showing both history (lighter blue) and futures markets (darker blue):

As noted in my earlier posts, oil and natural prices appear to have disconnected from their historical relationship. For many years, oil prices (as measured in $ per barrel) tended to be 6 to 12 times natural gas prices (as measured in $ per MMBtu). That ratio blew out to more than 20 in late 2009, then receded to more traditional levels, and then blew out again in recent months. At yesterday’s close, the ratio stood at 21.8, far above its historical range.

In my previous posts, I argued that this unusual pricing reflects the sudden (and welcome) increase in natural gas supplies and that we should expect oil and natural gas prices to eventually move back toward their historical relationship as markets absorb the new gas. Of course, I was careful not to say when this would happen.

As shown in the graph, the futures markets are indeed signaling some normalization in the price ratio in coming years, but not a rapid one. Moreover, even after eight years, the ratio would return only to the upper end (12) of its historical range. (Caveat: Futures markets are quite thin that far out, so we shouldn’t place too much weight on those distant prices.)

Let me offer a revised interpretation of the pricing relationship that’s consistent both with the futures data and the comments I received. This interpretation (consider it a theory, really) distinguishes four time periods:

- Good Old Days: For many years, the electric utility industry had generating plants that ran on oil, natural gas, or both. The ability to fuel switch (either by changing the dispatch order of oil and gas plants or changing fuels at plants that could use either) limited how much oil and natural gas prices could deviate. If oil prices fell too low, utilities would move from natural gas to oil, and vice-versa. Similar fuel arbitrage occurred, to varying degrees, among other uses as well (e.g., home heating and some industrial uses).

- More Recent Days: In recent decades, electric utilities have embraced natural gas and moved away from oil. As a result, there is much less opportunity for arbitrage between the fuels. The same has happened among other fuel consumers as well. Oil and natural gas prices nonetheless remained within their usual historical relationship. For example, oil and natural gas prices rose and fell in tandem during 2008. This suggests that the markets encountered similar shocks during those years (e.g., strong demand or, some would argue, speculation), not that they were linked via arbitrage.

- Today: With the decline of traditional fuel arbitrage possibilities, oil and natural gas prices can now move separately if they experience distinct shocks. That appears to have happened with the increase in natural gas supply, for example.

- Future: Looking further ahead, however, one would expect some new arbitrage relationships to develop. If we have persistently cheap natural gas and persistently expensive oil, that creates an incentive for ingenious folks to find ways to use natural gas to serve what have traditionally been oil demands. That should eventually limit the degree to which the prices can deviate (although not necessarily in the 6 to 12 ratio range). Two leading candidates for this linkage are using natural gas as a transportation fuel (directly as a fuel and perhaps indirectly as electricity) and increased international trade in liquified natural gas.

Note: The chart uses the spot price for West Texas Intermediate at Cushing and the spot price for natural gas at Henry Hub on a monthly basis through March 2010. For April 2010, I use the closing prices on April 8. The monthly futures are from the CME Group.

Add/view comments on this post.

------------------------------

The Christian Science Monitor has assembled a diverse group of the best economy-related bloggers out there. Our guest bloggers are not employed or directed by the Monitor and the views expressed are the bloggers' own, as is responsibility for the content of their blogs. To contact us about a blogger, click here. To add or view a comment on a guest blog, please go to the blogger's own site by clicking on the link above.