Jobless report: The good, the bad, the ugly

-

Jared Bernstein Guest blogger

Jared Bernstein Guest blogger

Re the job situation:

The Good:

–Payrolls expanded in every month last year, the first time we’ve seen that for a while, adding 1.6 million jobs overall and 1.9 million in the private sector (continued public sector job loss is one of the bads).

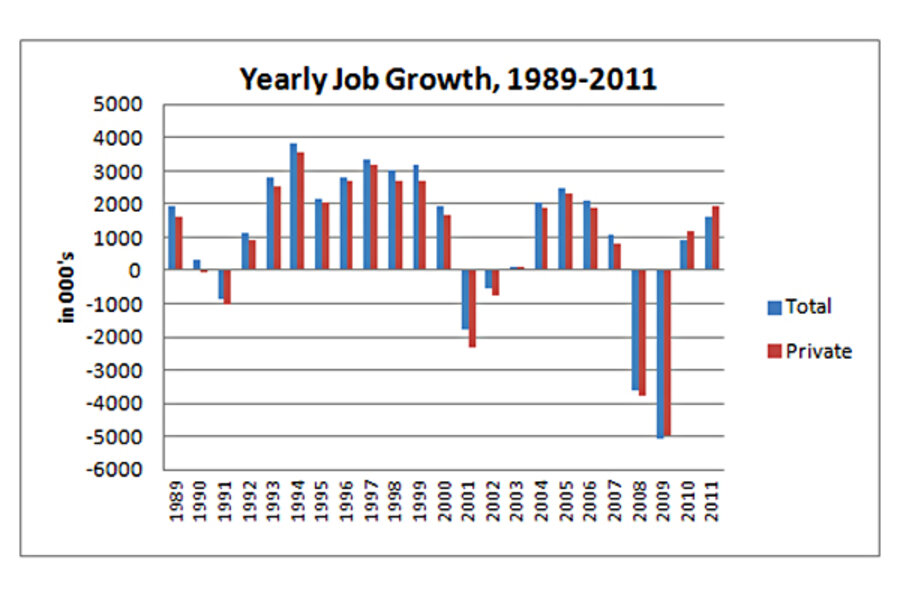

–The figure shows the annual growth (December/December) or loss of jobs over the last three business cycles: 1990s, the 2000s, and the nascent recovery that’s underway. The difference in job losses between the great recession and the prior two (1990-91 and 2001) is the first thing that jumps out at you. We’ve just got so much more ground to make up. But (hey—this is supposed to be the good part!) we are starting to make it up. Too slowly for sure, but the figure shows we’re climbing out of the trench.

The other thing you see in the above figure is just how weak the jobs recovery of the 2000s was—compared to the 1990s, there were precious few years of job growth—and pretty anemic ones, at that. So, one question posed by this chart is whether we’re at the beginning of a 90’s or 2000’s type of jobs recovery…and what policies will help generate the latter pattern over the former.]

–Unemployment is trending down. It peaked at 10% in Oct of 2010 and hit 8.5% last month. However, no small part of this decline is due to people leaving the labor force (see below).

–The underemployment rate is down 1.4 ppts from a year ago, from 16.6% to 15.2%, driven in part by the decline of almost 800,000 in the number of involuntary part timers (i.e., part-time workers who want full time jobs).

The Bad:

–Levels vs. Trends: On many of these labor market variables, the trend is our friend, the level bedevils. We’ve got some slow momentum going in job growth, but we’re still millions of jbos below the pre-great-recession peak. The jobless rate is down 1.5 percentage points off of its peak, but 8.5% is way too high on the level.

–Job Quality: Many of the jobs we’ve added over the past year have been in low-paying sectors, like restaurants, bars, and retailers (part of the 200K gain last month, e.g., included 42,000 jobs for couriers/messengers, presumably related to holiday deliveries). On the other hand, manufacturing’s picked up lately, up 225K over the year.

–Labor Force Participation: This is the most notable bad we face right now. The share of the working-age population either working or looking for work remains depressed, surely because a lot of people gave up the job search in an inhospitable environment. This makes the decline in unemployment look better than it really is, because once you leave the job market you’re not counted among the unemployed. It also means that once things pick up, some of those folks are going to get drawn back into the job search and that puts upward pressure on the jobless rate. I expect this to occur this year.

–Long Term Unemployment: Still a huge problem, with over 40% of the jobless unemployed for at least half a year. Again, it’s a testament to the mismatch between labor supply and labor demand, with the latter improving but still far too weak to meet the needs of those seeking work. And please, don’t blame extended UI (unemployment insurance) benefits for either this bad or the last bad (lower labor force participation). Re the former, we’ve just got too many jobseekers chasing too few jobs. Re the latter, you have to look for work when you’re on UI, and that rule is enforced pretty strictly.

–Public Sector: The state and local government sector continues to shed jobs, down about half-a-million over the last two years. They’re cutting budgets and taking it out of their workforces, and remember, these are teachers, police, sanitation workers—folks whose work is essential to our communities (education jobs at the local level are down 190K over the past two years).

The Ugly:

That would be Congress. As I said earlier, policy makers need to sustain and build upon the gains we’ve achieved thus far. Fiscal support is fading and the private-sector engine of job growth is still somewhere around first or second gear. Whether we slog along or build to a more robust recovery is at this point a function of whether these guys create more self-inflicted wounds, like failing to extend the payroll tax cut and UI benefits beyond two months. Or whether they respond to any forthcoming problems we can’t see yet—if Europe or oil or who knows generate new headwinds, it’s hard to imagine this Congress helping to offset them.

Stay tuned…